NEWS RELEASE January 2019

Cement Combust, Flow and Treat (CFT) Market will Exceed $50 billion in 2025

The cement industry has invested $400 billion to produce 4 billion tons of cement per year. Cement revenues are likely to grow at 6 %/yr over the next six years to reach $700 billion in 2025. Annual expenditures for combust, flow and treat products and services will exceed $50 billion per year.

The cement industry is one of the largest purchasers of air pollution control equipment and services. Historically plants needed only to comply with particulate emission regulations. Now HCl, SO2, VOCs and mercury are being regulated. The kerogen in the feed limestone along with other constituents vary within individual limestone deposits. As a result the quantity of pollutants to be removed varies from hour to hour. This is a challenge to operators.

Cement plants have transitioned to dry processing over the years. As a result the major purchases, are kilns, granular material handling and sizing, fans, dampers, dust collectors, and storage facilities. The valve purchases are mostly for air control purposes. Analyzer needs are to measure free flowing solids. The requirements for pumps and liquid analyzers are minimal.

The large cement producers operate many plants Holcim- Lafarge operates 220, Heidelberg operates 141 and Cemex operates 61. The fact that companies operate a number of plants in remote locations makes it desirable to centralize total cost of ownership evaluations of combust, flow, and treat equipment. It also makes IIoT and Remote O&M very cost effective.

The world cement industry is anticipating volume increases of 6% per year in the next three years versus less than 3% per year over the last three years. Profitability in 2018 was down due to overcapacity, rising cost of fuel and other factors.

The industry is steadily increasing its investment in IIoT. Instrumentation can instantly communicate the particle size distribution to the process management system which can then adjust the grinding regime to balance energy consumption and cement product quality.

The cost of capturing particulate is being reduced with bag designs which require less energy consumption. The need to also remove NOx and VOCs can be met with catalytic bags. Dry sorbent injection can be used ahead of the catalytic filter to remove acid gases. This reduces capital cost and energy consumption as compared to separate removal devices.

The cement industry can contribute to total pollution reduction with the combustion of sewage sludge, and other waste materials. This reduces the fossil fuel energy requirement and also results in better air pollutant capture as compared to technology often used for incinerating waste. The use of multiple fuels in varying amounts creates additional operational challenges and further justifies the investment in IIoT.

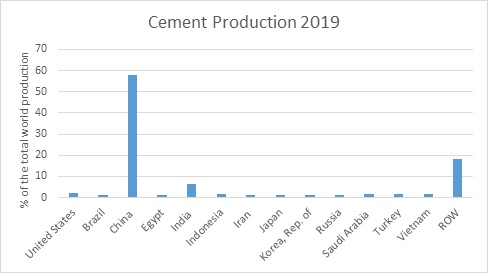

The industry continues to be dominated by China. India is the next largest producer. Forecasts of CFT purchases by the cement industry are provided in the following reports

N007 Thermal Catalytic World Air Pollution Markets

N008 Scrubber/Adsorber/Biofilter World Markets

N018 Electrostatic Precipitator World Market

N021 World Fabric Filter and Element Market

N027 FGD Market and Strategies

N056 Mercury Air Reduction Market

N031 Industrial IOT and Remote O&M

5AB Air Pollution Management

N026 Water and Wastewater Treatment Chemicals: World Market

N024 Cartridge Filters: World Market

N006 Liquid Filtration and Media World Markets

N005 Sedimentation and Centrifugation World Markets

For more information contact Bob Mcilvaine at This email address is being protected from spambots. You need JavaScript enabled to view it. 847 784 0012 ext 122